I found this article to be relevant! Many sellers feel the value of their home does is not impacted by cosmetic improvements or fall out from the recession. The value of a home IS affected by supply and demand as this article points out.

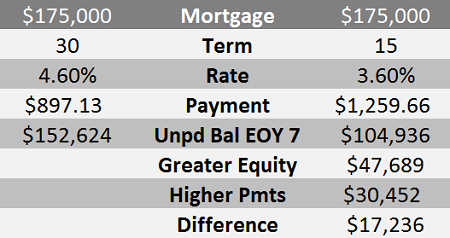

Look at the improved equity position on a 15-year mortgage vs 30-year mortgage. Equity is the difference in what your home is worth and what you owe. Ideally, as the value goes up and the unpaid balance goes down with each amortized payment made, the equity grows from two directions. This dynamic leads to increasing a person's net worth much faster than many other investments. A homeowner has minimal control over value. It is necessary to maintain the property to avoid depreciation and make good decisions on capital improvements. After that, appreciation is generally controlled by supply and demand and the economy. Mortgage management is something that the homeowner does have control. Making the decision to select a shorter term mortgage at a lower interest rate can have an impact on equity build-up. Lower interest rates amortize faster than higher interest rates which will also affect equity growth. Currently, it is possible to get a 1% lower rate on a 15-year mortgage than a 30-year mortgage. Compare two alternatives of a 30-year and a 15-year mortgage. The payments will definitely be higher on the shorter term because it pays off quicker. However, if a person can afford the higher payments of $362.53 more per month in this example, the equity will be greater. Even after you take into consideration the higher payments, the increased equity is $17,236 at the end of the seven-year holding period.

Another decision that can affect equity build-up is making additional principal contributions along with the regular payments. Whether you're making an occasional lump sum payment toward principal or regular monthly contributions, it will save interest, build equity and shorten the term on a fixed rate mortgage. Estimate your personal savings with this Equity Accelerator.

Connect