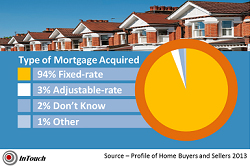

In 2013, the Types of Mortgages Acquired Shows the Trend...But Should You Follow Suit?

Fixed or Adjustable Rate - IT DEPENDS! 94% of purchasers last year opted for a fixed-rate mortgage at some of the lowest rates in home buying history. Yet, some of them will pay more in interest than necessary, based on the time theyll own the [...]

Connect